Summary

This paper goals to summarise and current the primary proposals of the Spanish White Guide on Tax Reform within the environmental area, a very essential chapter, amounting to round 15% of its whole content material. It attracted vital consideration from the general public resulting from its quite a few and impressive proposals, along with their detailed evaluation. The White Guide may be helpful for a global viewers, as Spain shares with different superior international locations many environmental issues and challenges related to the ecological transition and has a really comparable regulatory and tax construction. Furthermore, the environmental and distributional conclusions of the environmental chapter are notably related at instances of vitality and local weather crises.

Introduction

In April 2021 the Spanish Authorities commissioned a bunch of 17 consultants, principally professors of economics and legislation, to organize a White Guide (WB) on tax reform for the required adaptation of the Spanish tax system to the financial actuality of the 21st century. To this finish, the consultants had been requested to hold out an evaluation of the optimum tax system in a broad sense, evaluating facets such because the sufficiency, fairness and effectivity of the totally different sources of public income. Particular analyses had been additionally requested on environmental taxation, company taxation, taxation of the digital financial system and rising actions, and wealth taxation. The Authorities included the preparation of the WB, which was delivered in early March 2022 (CPELBRT, 2022), inside its plan and commitments to obtain the numerous funding from the EU Restoration and Resilience Facility to mitigate the financial and social impacts related to COVID.

In any case, it isn’t solely the detailed and in depth exploration of the function of environmental taxation in fixing Spain’s most important environmental challenges that may make this working paper fascinating for a global viewers. Spain shares with different superior international locations many environmental issues and challenges related to the ecological transition and has a really comparable regulatory and tax construction (extremely harmonised within the case of the EU). Subsequently, I consider that the conclusions offered right here may be extremely helpful past Spain’s borders.

The working paper is organised in 5 sections, together with this introduction. The second part comprises the chapter’s foundations and its analysis of the Spanish tax system on this area. What follows is a concise presentation of the rules and pointers that inform the WB’s environmental proposals. The fourth part particulars the primary proposals and the outcomes of their illustrative evaluation in 4 most important areas: electrification, transport, circularity and water. Lastly, the final part of this paper presents the primary environmental and distributional messages from the WB and highlights its relevance 9 months later, within the midst of intense and simultaneous vitality and local weather crises.

Environmental taxation in idea and follow

(2.1) Foundations

Environmental taxes are levies that goal to foster modifications within the behaviour and inventory (tools) of financial brokers (shoppers, producers) that may result in a discount of emissions and/or the usage of materials assets, thus reaching decrease environmental impacts. For this function, it will be needed for the environmental tax charges and base to be associated to the environmental injury or to contribute to reaching pre-established environmental targets. For the reason that taxes are designed to deal with adverse externalities of financial actions, it will thus be fascinating for his or her tax fee to be near the marginal exterior value of emissions, consumption or manufacturing. Nonetheless, as environmental insurance policies are normally set on the idea of emission discount targets in the actual world, environmental taxes may additionally be helpful on this setting resulting from their potential to realize these targets.

Environmental taxes have a number of benefits that make them a most popular choice for economists specialised in environmental coverage, explaining the educational insistence on their use and the curiosity of many worldwide organisations and suppose tanks. They’re devices that goal to ‘get the costs proper’ by complying with the ‘polluter pays precept’, main brokers to make acceptable selections. Since there may be normally an ideal heterogeneity amongst these inflicting environmental injury, in addition to issues of uneven data on prices and emission discount prospects between regulator and polluters, environmental taxes obtain enhancements at a minimal value as a result of, in contrast with different coverage alternate options, they permit brokers to adapt and thus cause them to mechanically reveal their prices and prospects of decreasing environmental impacts (Fullerton et al., 2010). In any case, these properties apply solely when all these inflicting the environmental downside face the value sign with the identical depth, which recommends avoiding sectoral exemptions and tax reductions.

Additionally it is essential to emphasize the salience that’s normally related to taxation (Rivers & Schaufele, 2015). Not like different coverage alternate options, environmental taxes typically convey a few clearer view of the prices and their distribution by teams of residents or by sectors, which facilitates the definition of compensatory measures to guard competitiveness or attainable adverse distributional impacts. Furthermore, there may be rising educational proof that the upper the salience of a coverage instrument, the stronger the response of brokers and thus its environmental effectiveness.

Moreover, the analysis of environmental taxes is crucial. This evaluation ought to ponder a number of standards, together with their environmental effectiveness (the extent to which they supply incentives to cut back emissions or useful resource use within the quick and lengthy phrases), their socio-economic impacts and their revenue-raising capability and distribution of burden by family group and financial sector (Gago et al., 2021a). Normally, the educational literature exhibits that environmental taxes obtain constructive environmental impacts, particularly in comparison with what would have occurred with out their introduction, have excessive cost-effectiveness, generate distributional impacts that strongly depend upon the context of software and the existence of compensatory measures, and would not have vital results on competitiveness. Nonetheless, they face vital obstacles, as they’re unpopular measures and topic to lobbying by trade (see Gago et al., 2014).

(2.2) Spain within the worldwide context

Environmental taxation performs a related function in tax methods across the globe, with revenues in 2019 accounting for 1.52% of GDP and 5.03% of tax income within the OECD (2021), in addition to 2.4% of GDP and 5.9% of tax income within the EU-27. Vitality taxes are the primary supply of environmental revenues within the EU-27 (78%), particularly these levied on transport fuels, whereas different transport taxes account for 19% of revenues and air pollution, whereas useful resource taxes account for less than 3% (European Fee, 2021b).

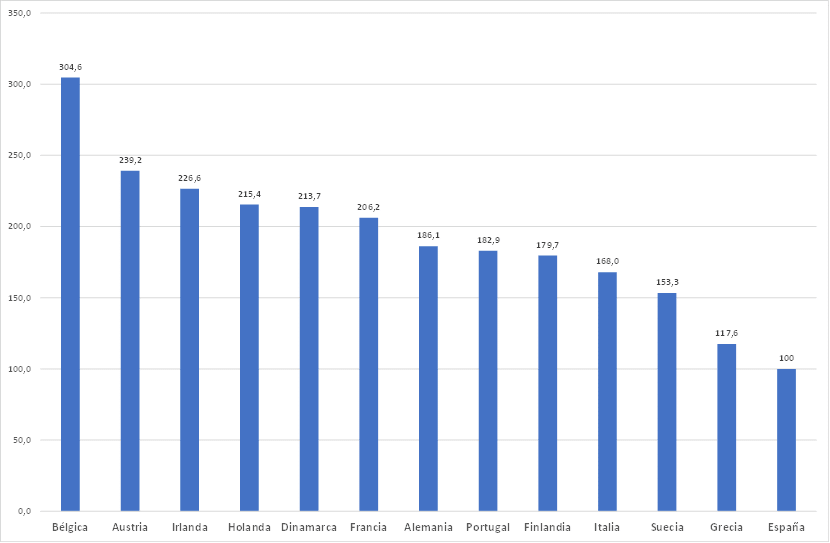

The WB pays explicit consideration to the present educational proof for Spain, typically by ex-ante simulations of the results of various environmental taxes. The sizeable literature typically exhibits a big effectiveness in correcting the environmental downside, with restricted financial and distributional impacts (Gago et al., 2021b). Moreover, there may be proof of the social acceptance of those figures (IEF, 2021), though there are divergences between totally different taxes and, normally, residents are in favour of proposals with a transparent environmental rationale and distributional compensations. Nonetheless, the Spanish expertise with these taxes exhibits a restricted variety of purposes in addition to –in lots of circumstances– a poor selection and tax design, which locations the nation on the backside of the EU classification in the usage of these taxes (Determine 1). Certainly, many environmental issues, polluting actions or sectors are usually not lined, and there’s a use of tax charges that don’t adequately mirror damages or contribute to the attainment of Spanish commitments within the area. Likewise, there may be extreme administrative complexity, scant linkage with environmental issues to right sure tax bases and an unequal and uncoordinated use of environmental taxes at totally different jurisdictional ranges.

Determine 1. Environmental income in relation to GDP, 2019

These issues have been repeatedly identified by the European Fee and lots of different worldwide organisations, calling on successive Spanish governments to undertake a extra proactive angle to environmental taxation however with little outcome to this point. Moreover, lately varied official skilled teams have been requested to supply a analysis of the state of affairs and to formulate proposals on this space, exhibiting up the lesser growth, design deficiencies and scant progress achieved over the last many years. Undoubtedly, this has negatively affected the flexibility of Spanish public insurance policies to cope with the damages and commitments related to rising environmental issues and is more likely to require extra intensive and in depth efforts within the area of environmental taxation.

Rules and pointers for Spanish environmental tax reform

Given the above-mentioned want to deal with the quantitative and qualitative issues of environmental taxation in Spain, a number of rules have guided the work of the skilled group to underpin and information the precise proposals of the WB.

(3.1) Environmental rationality

Environmental taxes must be understood as the required response to the excessive and rising vulnerabilities and impacts seen in Spain. Certainly, Spain is likely one of the superior international locations most affected by local weather change, which has essential implications as a result of dependence of many financial actions on environmental circumstances and pure assets (Eckstein et al., 2020). Native air pollution can be a persistent downside and the supply of main human well being issues in most city areas, whereas Spanish biodiversity is threatened by human-induced disruptions.

That is the primary context for deciding which environmental taxes to prioritise and the depth of their software. Determine 2 exhibits a number of the environmental targets to which Spain has legally dedicated itself, typically as a consequence of EU insurance policies and techniques, to permitting a roadmap to be drawn up exhibiting the priorities and timing of the required reforms. Particularly, it highlights the necessity for motion on greenhouse gasoline (GHG) emissions, particularly within the so-called diffuse sectors (not topic to the EU emissions buying and selling system or ETS), and on different related pollution which can be generated by transport and agriculture. There are additionally vital discrepancies between the commitments adopted and the present state of affairs in stable waste, whereas in water there’s a clear incapability to get well the prices related to its use.

Determine 2. Spain’s environmental commitments

| Environmental downside / Reference yr | Goal | Evolution |

|---|---|---|

| 1. Greenhouse Gasoline Emissions (GHG) / 1990 | -23% in 2030 | +8.5% (2019) |

| 1b. GHG emissions diffuse sectors/2005 | -26% in 2030 (-37.7% in 2030, Match for 55) | -15.1% (2019) |

| 2. Emissions of Nitrogen Oxides (NOx) / 2005 | -41% between 2020-29 -62% from 2030 | -50.3% (2019) |

| 3. Emissions of Unstable Natural Compounds aside from Methane (NMVOC) / 2005 | -22% between 2020-29 -39% from 2030 | -23.3% (2019) |

| 4. Ammonia (NH3) Emissions / 2005 | -3% between 2020-29 -16% from 2030 | -2.8% (2019) |

| 5. Particulate Matter 2.5 (PM2,5) Emissions / 2005 | -15% between 2020-29 -50% from 2030 | -8.6% (2019) |

| 6. Vitality effectivity (Mtoe) | Major vitality: 122.6 (2020); 98.5 (2030) Closing Vitality: 87.23 (2020); 73.60 (2030) | Major vitality: 120.75 (2019) Closing vitality: 86,30 (2019) |

| 7. Weight of waste produced / 2010 | -10% in 2020 -15% by 2030 | -8.1%* (2018) -6.9%** (2018) |

| 8. Family and comparable wastes destined for preparation for reuse and recycling | 50% by 2020 | 35%*** (2018) |

| 9. Non-hazardous development wastes destined for preparation for reuse and recycling | 70% in 2020 | 47%**** (2018) |

| 10. Restoration of the prices of water-related providers | 100% | 67,9% |

Sources: CPELBRF (2022) from MITECO, Inventario Nacional de Emisiones a la Atmósfera; INE, Estadísticas sobre Recogida y Tratamiento de Residuos; MITECO, Memoria Anual de Generación y Gestión de Residuos; European Fee, Fee Evaluation for Spain’s NECP; Eurostat, Vitality Effectivity; and MITECO, Síntesis de los Planes Hidrológicos Españoles. WFD Second Cycle (2015-2021).

Proposals for the reform of environmental taxation in Spain

As indicated, the WB’s environmental tax proposals are grouped in 4 basic sections that incorporate a basic reflection on the usefulness of taxes to cope with the precise environmental downside, an outline of present taxes within the space in Spain and a abstract of the accessible empirical literature. This process supplies a foundation for the proposals and their analysis, as proven within the following subsections.

(4.1) Sustainable electrification

As identified, the supply and rising deployment of mature renewable applied sciences within the electrical energy sector makes this sector key to the ecological transition, notably in decarbonisation. To allow the transition to a low-carbon financial system, the electrification of different sectors during which the event of renewable energies is proscribed, reminiscent of transport, will likely be important. Environmental taxation ought to favour this course of by differentiating vitality sources in line with their environmental profile, selling technological growth and investments that allow widespread electrification. To attain this, the environmental taxes levied on electrical energy in its totally different phases (technology, distribution and consumption) must be reformed to align them with three basic targets for the ecological transition: electrification (changing fossil fuels with renewable electrical energy); selling vitality effectivity; and decreasing the adverse environmental impacts related to electrical energy technology.

At current, the Spanish authorities levies totally different taxes on electrical energy technology, together with the tax on the worth of electrical energy manufacturing (IVPEE), which is levied on the manufacturing and incorporation of electrical energy into the system, taxes on the manufacturing and storage of radioactive waste, and the tax on the usage of inland waters for electrical energy manufacturing, which is levied on the worth of the hydroelectric vitality produced. There are additionally a number of regional taxes on electrical energy technology and distribution (taxes on installations, water reservoirs, atmospheric emissions, wind vitality and electrical energy technology). Taxes on electrical energy consumption embrace the (harmonised) excise tax on electrical energy (IEE) and VAT on the basic fee.[1] On account of these figures, the tax burden on electrical energy in Spain has historically been larger than the EU common for households, however decrease for trade (Eurostat, 2021a).

On this context, the precise proposals to favour the ecological transition within the electrical energy sector can be the suppression of the IVPEE, the modification of the IEE, the introduction of measures to enhance the design and effectiveness of regional taxes on this space and the protection of all prices related to nuclear energy vegetation.

The IVPEE was launched with the goal of decreasing the pervasive electrical energy sector deficits and it doesn’t promote technological change in electrical energy technology (because it doesn’t discriminate between applied sciences in line with their environmental impacts), and it hinders electrification by rising relative electrical energy costs. Thus, its solely environmental advantages derive from its constructive results on vitality effectivity, which may be achieved with the IEE. Utilizing electrical energy consumption information from CNMC (2020), in addition to electrical energy value information from Eurostat (2021a) and the electrical energy value elasticity estimated for Spain by Labandeira et al. (2016).

(4.2) Mobility suitable with the ecological transition

The transport sector generates vital adverse externalities that must be corrected by public intervention. These embrace GHG emissions and native air pollution, but additionally the prices of congestion, accidents, noise or infrastructure, which collectively account for round 5% of GDP in developed international locations (van Essen et al., 2019). To regulate these externalities, there are quite a few regulatory choices, however taxation can play a key function by incentivising behavioural modifications and investments in clear applied sciences. Furthermore, the existence of heterogeneous actors and a number of tax alternate options supplies an acceptable context for environmental taxation on this case. That’s the reason environmental tax reforms must be aimed toward incorporating the externalities related to transport, facilitating compliance with environmental targets at minimal value, the place modal shift ought to play a key function by incentivisation of much less polluting alternate options.

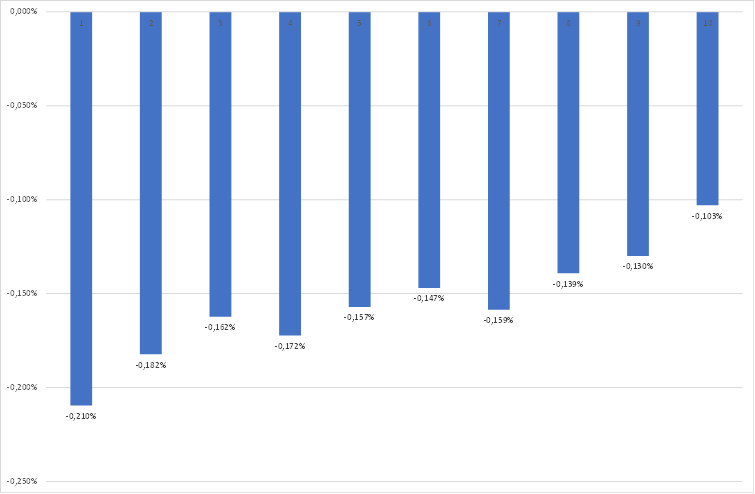

Spanish taxation on transport contains: the EU-harmonised excise tax on hydrocarbons (IEH), which is levied on motor fuels along with different fossil fuels reminiscent of pure gasoline; the tax on sure technique of transport (IEDMT), which is levied on the primary registration of autos in Spain; and the municipal tax on autos (IVTM), which is levied yearly on the possession of mechanical traction autos. As well as, Catalonia levies taxes on CO2 emissions from motor autos and on nitrogen emissions from aviation. In any case, Spanish taxes on motor fuels are effectively under the weighted EU-27 common, whereas taxation on automobile buy and possession was additionally comparatively low. As Determine 3 exhibits, as soon as once more this locations Spain on the backside of the EU rating by way of the overall tax burden on autos. Furthermore, the typical income per automobile has been considerably lowered because the mid-2000s, in order that the present state of affairs is neither justifiable nor sustainable, making an allowance for the significance of each the externalities related to transport and the general public revenues from this sector, and requires short-term motion on present taxes, in addition to a complete reform within the medium time period, introducing taxes on precise automobile use (Gago et al., 2019).

Determine 3. Common income per automobile in EU international locations, 2019 (Spain = 100)

Supply: CPELBRT (2022).

On this context, it will first be advisable to extend the excise tax fee for diesel to equal that of petrol. Utilizing information on gasoline consumption (CORES, 2021) and gasoline costs (MITECO, 2021a) in Spain in 2019, in addition to value elasticities from Labandeira et al. (2016), Determine 4 exhibits that the proposal would scale back emissions and generate vital further income, though it will have a regressive affect on households. Nonetheless, if the income is used to compensate households within the lowest 5 revenue deciles in order that, on common, these households are usually not affected by the reform, solely 8.1% of the extra income generated can be wanted to realize this.

Secondly, the WB recommends a basic enhance within the taxation of hydrocarbons, specifically on motor fuels and pure gasoline.[2] On this respect, in addition to equalising the excise duties of diesel and petrol, a further carbon value must be contemplated along with the impacts from the Nationwide Fund for the Sustainability of the Electrical energy System (FNSSE).[3] Within the case of pure gasoline, along with introducing the carbon value and the FNSSE, the share of the IEH might be raised to the minimal of the ETD proposal (€0.9/GJ).

Determine 4. Distributional affect of the equalisation of petrol and diesel taxes by equal revenue deciles

In any case, the measures would even have a big affect on sure financial actions, so it will be advisable to implement the reform step by step, to restrict its affect on inflation and GDP, and to make use of a part of the income to incentivise a metamorphosis that’s suitable with the ecological transition of probably the most affected sectors. Within the case of pure gasoline, it will be advisable to make use of a part of the income to encourage the event and implementation of much less polluting applied sciences (biogas, inexperienced hydrogen, and many others) to guard the competitiveness of the economic sector.

The WB additionally recommends actions to introduce environmental variables into the IVTM, in order that it contributes to an earlier substitute of extremely polluting autos by clear alternate options. To this finish, its design might be modified from levying the tax on the so-called fiscal energy to the usage of indicators of environmental injury, reminiscent of their environmental class (Euro), the official environmental classification labels of autos, or their stage of CO2 emissions.

However, present taxes on transport are at present ineffective in tackling congestion and native air pollution, that are a big a part of the adverse externalities related to highway transport, notably in city areas. It could subsequently be advisable to introduce a automobile tax that varies in line with time of day and site, relying on the quantity of visitors. Such a tax would scale back pointless journeys, producing vital advantages for customers who actually need entry to congested areas. Nonetheless, this cost might have regressive impacts, because it doesn’t bear in mind the financial capability of every driver, which might be mitigated by earmarking a part of the income for public transport enhancements (Fageda & Flores-Fillol, 2018). With respect to highway infrastructure prices, though the environmental taxes thought-about above can contribute to their protection, pay per use methods are extra environment friendly and clear approaches to this finish. Subsequently, it will be advisable to contemplate the introduction and extension of expenses for the precise use of sure transport infrastructures.

(4.3) Elevated circularity

The so-called round financial system is a mannequin of sustainable socio-economic growth that goals to cut back the linear move of supplies in manufacturing and consumption processes, by extending the helpful life and relocating waste from the tip of the provision chain to the start. On this context, lots of the tax proposals on this space goal to minimise materials use and waste by reinforcing re-use and recycling. Contemplating circularity as a basic technique to cut back materials use and environmental degradation, different tax proposals are included on this part.

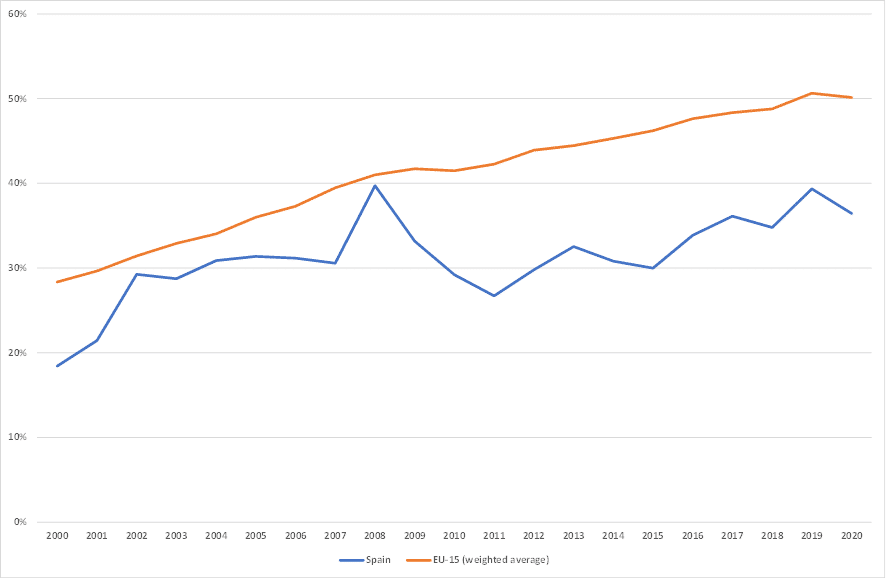

In Spain’s case, there are a collection of commitments within the area of the round financial system that in lots of circumstances are removed from being fulfilled and though municipal waste has been lowered lately its therapy has not improved considerably, in order that the extent of recycling is way from the European common because the starting of the century (Determine 5), whereas the share of waste that results in landfills (48.2% in 2018) is effectively above the EU common (38.5%) (Eurostat, 2021b).

Determine 5. Share of municipal waste recycled in Spain and EU-15, 2000-20

Supply: CPELBRT (2022) from Eurostat (2021b).

On this context, given the restricted effectiveness of the regulatory approaches utilized to this point to waste and the usage of supplies, it’s advisable to reformulate the methods and devices to realize Spain’s environmental targets. Inside insurance policies for making progress within the round financial system, taxation is a key instrument resulting from its capability to supply incentives for brokers to cut back waste and the usage of supplies. Thus, the precise tax proposals to favour the round financial system encompass the intensification and extension of the LRySC taxes, the reformulation of municipal waste taxation to hyperlink it to pay-as-you-throw methods, the creation of a tax on mixture extraction, the introduction of a tax on nitrogen fertilisers, and the extension and harmonisation of taxation on sure emissions from giant industrial and livestock services.

Nitrate air pollution from agriculture, attributable to an extreme use of fertilisers, is a vital environmental externality in Spain. As it’s diffuse air pollution, it’s tough to establish the reason for the issue, so the introduction of a mineral nitrogen tax might result in a second-best resolution (Jayet & Petsakos, 2013). Subsequently, the WB proposes the implementation of a tax on the nitrogen contained in sure fertilisers in order that a part of the environmental prices are integrated of their value, discouraging the abusive use of probably the most dangerous fertilisers and favouring much less polluting choices. Furthermore, provided that these merchandise take pleasure in a lowered VAT fee in Spain, it will even be fascinating to boost it (in keeping with different proposals of the WB relating to oblique taxation). In any case, a gradual introduction of this tax can be advisable in an effort to keep away from vital impacts on the agricultural sector, in addition to the appliance of compensatory mechanisms and an enough transmission of the correction of environmental prices to shoppers.

Lastly, there are particular atmospheric emissions which have vital impacts on local weather change, human well being, ecosystems and infrastructures. The emitters of those pollution embrace giant industrial services and livestock farming (particularly intensive livestock farming), and it will subsequently be advisable to introduce a tax on NOx, CH4, CO, NH3, COVDM and N2O emissions attributable to giant industrial complexes, in addition to CH4, NH3 and N2O emissions from intensive livestock farming.[5] Utilizing information from MITECO (2021b), making use of a tax fee equal to 1 fifth of the environmental injury of every pollutant as calculated by CE Delft (2018) and assuming that brokers don’t react to taxes, Determine 12 exhibits that such a measure would generate vital revenues (word that environmental and value results are usually not calculated as a result of lack of knowledge). But a gradual introduction of this tax and a partial income refund can be advisable to facilitate the adoption of cleaner applied sciences. Tax rebates primarily based on the usage of greatest accessible expertise or greatest working methods would even be fascinating.

Determine 6. Emissions, tax fee and income from emission taxation of enormous industrial websites and intensive livestock farming

| Pollutant | Emissions (tonnes) | Tax fee (€/kg) | Revenues (€ mn) |

|---|---|---|---|

| NH3 | 2,783.50 66,449.4 | 3.5 | 9.74 232.57 |

| COVDM | 52,925.07 | 0.23 | 12.17 |

| CH4 | 165,640.36 232,380.2 | 0.348 | 57.64 80.87 |

| CO | 261,026.34 | 0.011 | 2.75 |

| N2O | 2,220.21 987 | 3 | 6.66 2.96 |

| NOx | 178,012.09 | 2.96 | 526.91 |

| Complete | 810,740.56 | – | 615.88 316.41 |

Supply: CPELBRT (2022).

(4.4) Incorporation of environmental prices related to water use

Issues associated to the supply of high quality water are notably severe and have an effect on important socio-economic sectors in Spain, producing vital environmental impacts. Certainly, Spain is likely one of the most arid international locations within the EU, with a excessive diploma of water stress, with droughts and durations of shortage, issues which can be being aggravated by local weather change. Nonetheless, per capita water consumption in Spain is among the many highest within the EU, primarily resulting from its use within the agricultural sector.

Water governance in Spain is especially complicated, because it entails totally different administrative ranges that generally act in an uncoordinated method, leading to a excessive diploma of heterogeneity between territories, which, though fascinating as a result of excessive regional disparities, can generally result in unjustified and inefficient variations in laws and costs. Water administration within the EU is predicated on the appliance of the EU Water Framework Directive, which establishes the precept of restoration of the prices of water-related providers, together with environmental prices and people associated to water assets, as a key component within the definition of water coverage. Nonetheless, the diploma of restoration of the price of water providers is under 70% in Spain. On this context, the European Fee (2019) really helpful Spain ought to attempt for value restoration primarily based on the ‘polluter pays’ precept to make sure sustainable water administration.

The idea of the water tax regime in Spain has not been modified because the 1985 Water Legislation. At current, state water taxes embrace taxes on the usage of the general public area (tax on the occupation, use and exploitation of public water property and tax on the occupation of the maritime-terrestrial public area), taxes to get well the price of water infrastructures (regulation tax and water use tariff) and the discharge management levy. As well as, most Spanish areas have launched their very own taxes on taxable occasions linked to the totally different phases of the water cycle, primarily within the sanitation and discharge therapy phases. In lots of circumstances, native authorities apply expenses and tariffs for the provision and therapy of wastewater.

Dialogue and implications

Many issues have modified because the structure of the Spanish skilled group for the WB on tax reform in early 2021. The IPCC (2022) accomplished its 6th Evaluation Report, which supplies a worrying image of the sizeable impacts of local weather change and the shortcomings of mitigation methods the world over. A Summer time of report temperatures within the Northern hemisphere, nonetheless with GHG concentrations effectively under these of 1.5ºC ranges, additionally pointed to the urgency of taking motion. Notably, after rising value tensions from mid-2021, a extreme vitality disaster absolutely exploded following the Russian invasion of Ukraine.

On this context, are the vitality and environmental proposals of the WB nonetheless legitimate? Many Spanish policymakers, trade representatives and commentators thought that the environmental chapter of the WB had been born lifeless and was not relevant in the actual world. 9 months after its presentation, I consider that lots of its options are nonetheless absolutely legitimate to combat the vitality and local weather crises and to successfully defend these badly affected by the vitality value spiral.

Certainly, in a context during which main vitality tensions mustn’t endanger the environmental agenda but additionally supply new causes to speed up the ecological transition, energy-environmental taxation is bolstered in its function to incentivise extra vitality effectivity and a bigger deployment of non-fossil alternate options. Moreover, the present disaster additionally exhibits the pressing want for well-designed and everlasting measures to mitigate the distributional impacts generated by rising vitality costs. In sum, two main contributions of the WB as summarised on this paper.

The WB and this working paper have additionally confused the necessity for compensatory packages related to extra stringent environmental and local weather insurance policies. The WB suggests {that a} stable and lasting compensatory system for the ecological transition must be made up of transfers that aren’t linked to decrease fossil gasoline costs and are usually not generalised, supporting solely households under a sure stage of revenue. Additionally it is handy to strengthen these compensations with non-generalised programmes that speed up the change of kit, once more facilitating the adoption of unpolluted applied sciences for these teams with restricted entry to capital.

Sadly, as in most EU international locations, the Spanish authorities has launched options far faraway from the WB’s proposals within the vitality and environmental area. Generalised subsidies on polluting items are certainly towards the corrective wants of environmental and local weather insurance policies and are additionally imperfect compensatory gadgets. In Labandeira et al. (2022) we offer empirical proof on the a number of environmental, vitality, public expenditure and distributional shortcomings of such offsetting insurance policies, making them clearly inferior to these instructed by the WB.

[1] The federal government has suspended the appliance of the IVPEE on a number of events since 2018, whereas the Supreme Court docket has annulled a part of the regulation of the tax for the usage of inland waters for electrical energy manufacturing. Since 2021 the federal government has established momentary measures to cut back the extent of the above-mentioned taxes as a part of the packages to combat the vitality disaster.

[2] Though pure gasoline is simply marginally utilized in transport, it’s included on this part resulting from its presence within the new ETD.

[3] The simulated (€50/t) carbon tax intends to seize the results of the Match for 55 new emissions buying and selling system for transport and buildings. The FNSSE, at present beneath parliamentary process, goals to switch the mounted prices of the precise remuneration regime for renewable, cogeneration and waste services, related to earlier methods for the promotion of renewables, to all operators within the vitality sectors.

[4] Solely the IEDMT must be maintained to make sure that buying selections of autos are suitable with the in depth efforts to cut back adverse externalities.

[5] As talked about above, a number of areas apply their very own taxes on a few of these emissions, so the tax might set minimal tax charges giving areas the regulatory energy to extend them.

Picture: City orb. Picture: Joshua Rawson-Harris (Unsplash).